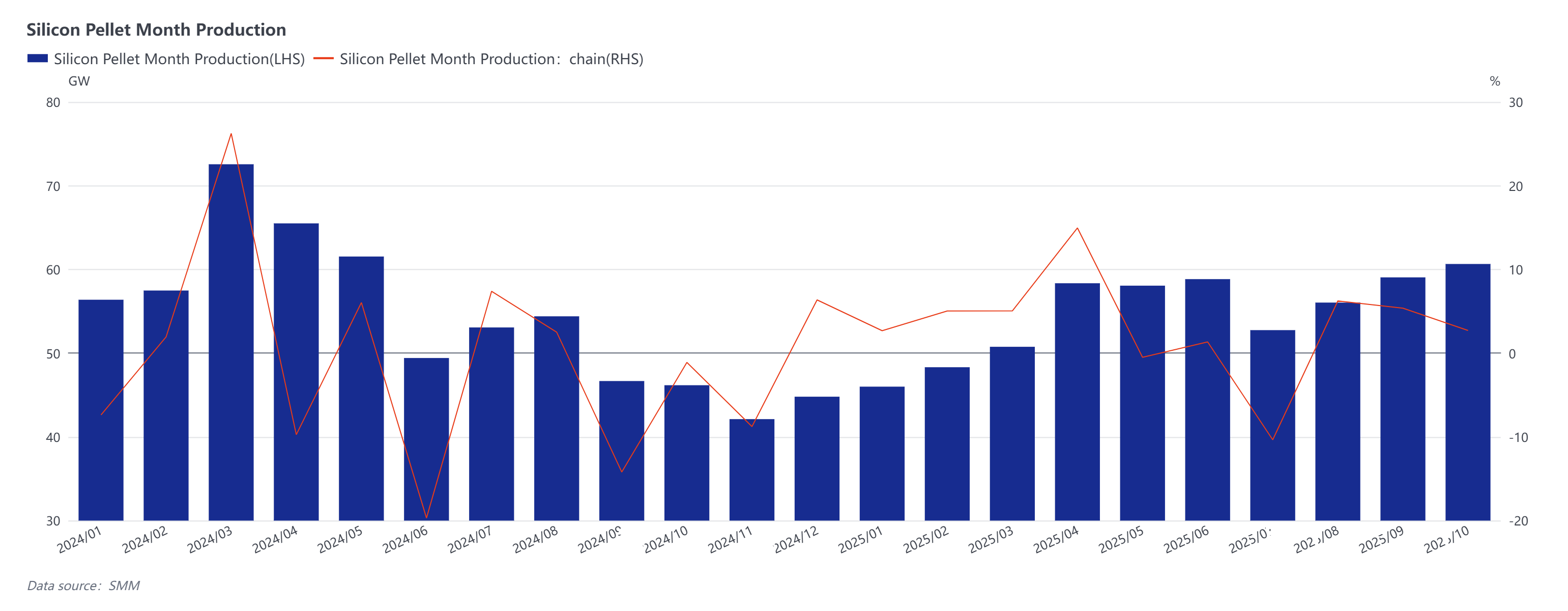

Two Top-Tier Enterprises Took the Lead in Production Cuts to Stabilize the Supply Landscape

According to SMM statistics, the two enterprises reduced production by a total of 1.95 GW in November, while other enterprises collectively cut production by only about 1 GW. Silicon wafer production in November is expected to be in the range of 57–58 GW, with little change from the production schedule anticipated at the beginning of the month. It has become a near-certainty that demand conditions deteriorated in the fourth quarter of this year, prompting the two leading enterprises to initiate production cuts to stabilize the supply landscape.

Excess Low-Priced Toll Processing Orders Are the Root Cause of Rapid Price Declines

According to SMM statistics, in November alone, the proportion of silicon wafers outsourced by battery manufacturers for toll processing accounted for more than 10% of total silicon wafer shipments (of which 3,000 mt were processed into silicon rods, with the remainder involving crystal pulling and slicing). While 10% may seem relatively small, it represents the actual volume of orders lost by silicon wafer manufacturers. Moreover, surveys indicate that a significant portion of these orders were processed at a loss—toll processing fees were essentially zero, forcing smaller silicon wafer enterprises to accept such contracts to maintain cash flow. These excess low-priced toll processing orders became the final straw, driving prices down by 3%–5% across three wafer sizes.

Several Silicon Wafer Enterprises Jointly Hold Prices Firm

On November 13, multiple silicon wafer enterprises jointly held prices firm, with the lowest prices for 183 and 210R wafers reported at 1.3 yuan/piece, while prices for 210N wafers remained unchanged. SMM analysis suggests that this joint effort represents a positive attempt at "anti-involution" in the PV industry, reflecting a growing consensus for rational competition. How to advance "anti-involution" has become a hot topic within the PV sector. In my view, other segments of the PV industry could follow the example of polysilicon by pursuing capacity integration. The goal of capacity integration is to facilitate orderly exits for enterprises, avoiding excessive competition that could weaken China's own strength. Additionally, new cooperation models between traders and enterprises could be developed, leveraging advanced financial tools to provide services that significantly reduce inventory pressure faced by enterprises in the circulation process.

![[SMM PV News] Armenia Hits 1.1 GW Solar Capacity,](https://imgqn.smm.cn/usercenter/qQwIB20251217171741.jpg)

![Spot Market and Domestic Inventory Brief Review (February 5, 2026) [SMM Silver Market Weekly Review]](https://imgqn.smm.cn/usercenter/tSwaX20251217171735.jpg)